Europe’s competition authorities have launched an in-depth investigation into Nike’s Dutch tax arrangements, first revealed in ICIJ’s Paradise Papers reporting.

The probe is likely to be one of the most significant launched by the European Commission and, if it results in a finding against Nike, could lead to the sportswear maker being forced to pay billions of dollars in back taxes to cover under-payments stretching back to 2006.

This would be many times the amount recovered from Amazon, Starbucks and Fiat following similar tax-related European Union competition probes. However, it would still be far short of the record-breaking $16.5 billion (€14.3 billion) in Irish back taxes recovered from Apple — another company that featured in ICIJ’s Paradise Papers reporting.

Responding to news of the Nike investigation, the company said: “We believe the European Commission’s investigation is without merit.” It added that Nike was “subject to, and rigorously ensures that it complies with, all the same tax laws as other companies operating in the Netherlands.”

After more than a decade of aggressive profit-shifting, by May 2017, Nike’s financial statements showed it had amassed $12.2 billion in foreign earnings, parked offshore. Much of this income had been shifted out of Europe before it could be taxed, ICIJ investigations found.

How Nike’s Dutch tax avoidance mechanism worked

Selling running shoes and other goods across Europe, Nike immediately pooled the resulting income in the Netherlands. Then, in a second step, it used large royalty payments to push a lot of that same income onwards, into other Nike subsidiaries that were not subject to tax at all.

The European Commission’s investigation will examine five tax rulings dealing with these controversial royalty payments. The rulings were granted to Nike by the Dutch tax authorities over many years. Two of them are still in force.

Lots of countries provide confidential tax rulings to multinational corporations to help such companies understand how their subsidiaries will be taxed locally.

But some EU countries — including the Netherlands, but also Luxembourg, Ireland and Belgium — have used rulings to secretly provide sweetheart tax deals to businesses that locate their European headquarters locally.

The Commission said: “[Our] investigation will focus on whether the Netherlands’ tax rulings endorsing these royalty payments may have unduly reduced the taxable base in the Netherlands of Nike European Operations Netherlands BV.”

It pointed out that while Nike’s Dutch subsidiaries had more than 1,000 employees, the royalty payments were made to subsidiaries that had no employees and no economic activity.

In response to the Nike investigation, the Dutch government said: “This does not mean that the Commission has already reached a verdict, but merely that they have doubts whether or not there was state aid. Of course we will fully support the work of the Commission.”

Tax rulings should “do nothing else than give certainty in advance on the application of tax laws, and should not lead to preferential treatment,” it added.

Nike routed payments to tax haven

In November 2017, ICIJ reporting revealed how Nike’s first tax ruling, in 2006, allowed large royalty payments to be made from Nike in the Netherlands to a subsidiary in the tax haven of Bermuda.

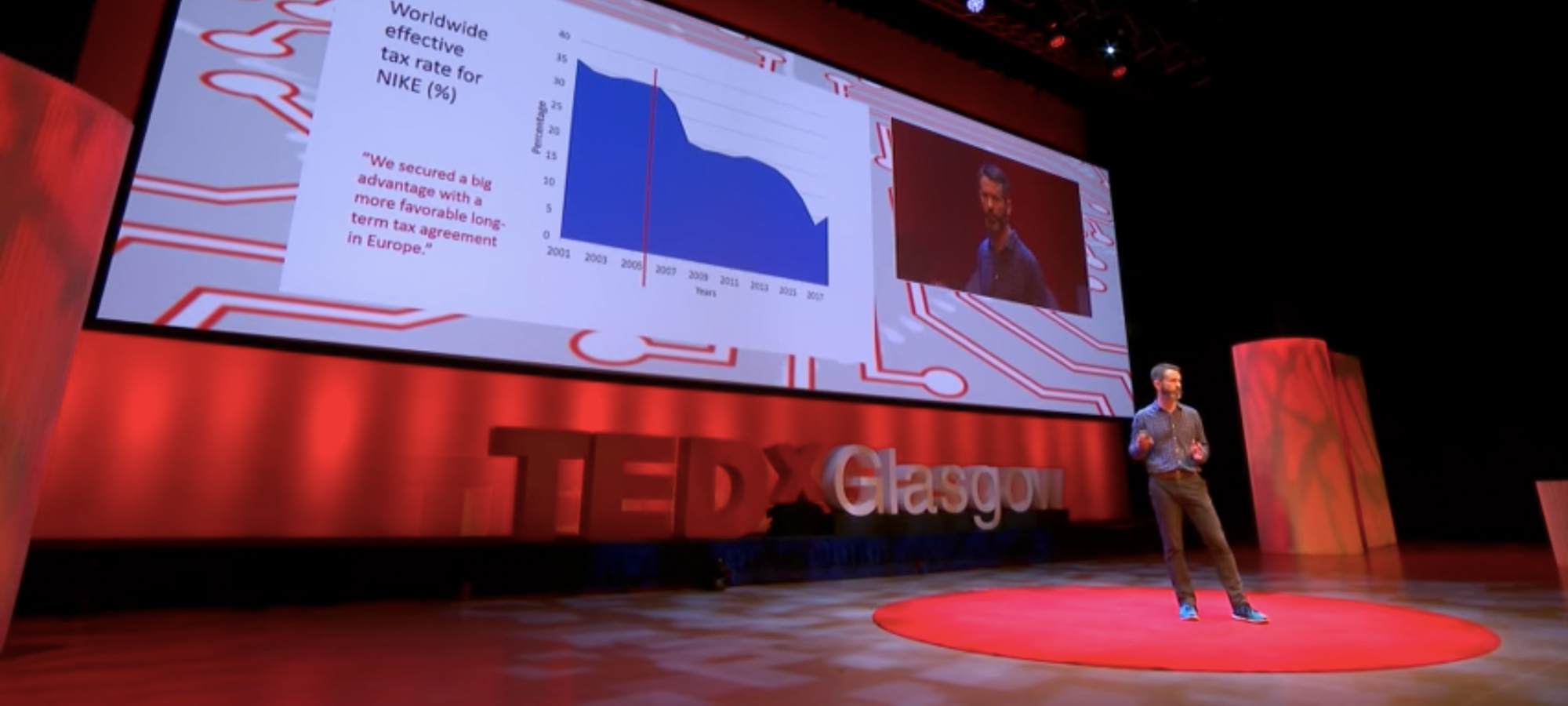

This had a swift and dramatic effect on Nike’s financial performance, cutting the group’s tax bill and boosting returns to stockholders, a pattern that has continued ever since. Despite this significant impact, chief executive Mark Parker only briefly referred to Nike’s Dutch tax rulings in a 2006 conference call with Wall Street analysts.

He said Nike had won “a more favorable long-term tax agreement in Europe,” according to a transcript of the call. This had, he added, “secured a big advantage.”

Now, EU Competition Commissioner Margrethe Vestager has launched an investigation into whether this advantage amounted to a sweetheart tax deal that secretly gave the sportswear maker an illegal advantage over competitors in European markets.

If so, the tax ruling would violate European competition laws designed to prevent EU member states from providing state aid to favored companies.

“Member States should not allow companies to set up complex structures that unduly reduce their taxable profits and give them an unfair advantage over competitors,” Vestager said. “The Commission will investigate carefully the tax treatment of Nike in the Netherlands, to assess whether it is in line with EU state aid rules.”

In June last year, Nike’s chief tax officer Patti Johnson gave evidence to a committee of the European Parliament, which was conducting a follow-up investigation in the wake of the Paradise Papers.

She denied there was anything artificial about Nike’s tax arrangements, saying: “Nike’s tax structure reflects our business structure. It is designed to facilitate the delivery of our products and services in the most efficient and cost-effective way to our consumers.”

The ‘ghost companies’ of the Netherlands

As ICIJ reporting showed, Nike’s Dutch units stopped making royalty payments to Bermuda in 2014, but went on to pay similar royalties to another subsidiary — this time a specially configured Dutch entity, called Nike Innovate CV, that was not subject to tax at all.

These kinds of subsidiaries, sometimes called “ghost companies,” are a common feature of tax avoidance arrangements for multinationals because they are not tax-resident anywhere the world.

As part of its Paradise Papers reporting, ICIJ reviewed stock market filings for America’s 500 largest publicly traded multinationals, using data available in June 2017, and found 214 subsidiaries that were formed as Dutch CVs.

The Netherlands has pledged to stop multinationals using CVs in tax avoidances arrangements, but the necessary reforms are not yet in effect.

Europe’s tax probes intensify after Paradise Papers

The commission has no direct powers to police the tax rules of EU member states but since 2013 it has increasingly been using its ability to challenge illegal state aid as a way of combating tax avoidance in Europe.

The Commission will investigate carefully the tax treatment of Nike in the Netherlands, to assess whether it is in line with EU state aid rules.

As part of this process, the commission has requested several member states share with competition investigators all confidential tax rulings granted to multinational companies. This has led to several full-blown probes, with more expected to follow.

In an emailed statement, a commission spokesperson told ICIJ: “The commission had already received some information on [Nike] rulings in the course of its overall investigation on tax rulings practices in all Member States before the Paradise Papers were leaked. Following the Paradise Papers allegations, the Commission intensified its investigation and requested additional information from the Netherlands, which led to the doubts the Commission is expressing in its opening decision of today.”