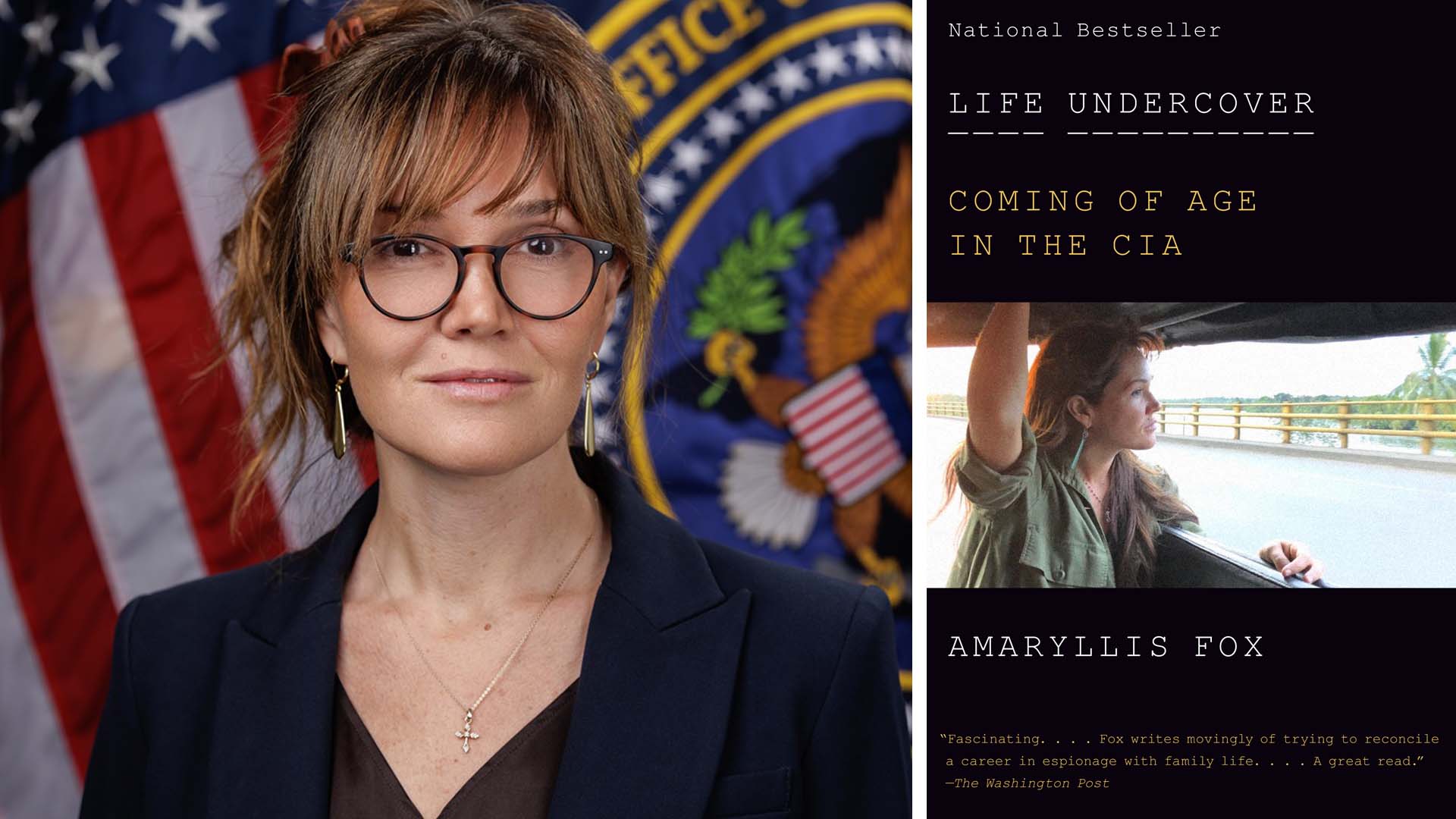

OFFSHORE

Trump intelligence adviser previously helped father pursue millions from Kremlin-linked bank, leaked documents show

Amaryllis Fox Kennedy, who recently stepped down from two senior administration posts, was serving as a CIA officer during the dispute.